Domestic Reverse Charge For The Construction Industry

What is it?

Domestic reverse charge (DRC) is a new way of accounting for VAT, it will apply to all VAT registered construction businesses in the UK. The new legislation is being introduced as an anti-fraud measure, it intends to cut down on the ‘missing trader’ fraud, where companies receive high net amounts for VAT from their customers but have no intention of paying the VAT to HMRC.

From Monday 1 March 2021 the domestic VAT reverse charge must be used for most supplies of building and construction services.

The charge applies to standard and reduced-rate VAT services:

- for individuals or businesses who are registered for VAT in the UK

- reported within the Construction Industry Scheme

What does it mean for you?

Firstly, please do not panic, put simply, the new legislation moves the VAT liability from the supplier (subcontractor) to the customer (contractor) but also not always, only if certain criteria is met, so please read on and we hope this document helps. There is a lot of information included here, so please do not hesitate to contact us if a call would be useful.

If you are a CIS subcontractor you will no longer charge VAT to your CIS customers. Instead, on your invoices you need to state your customer is responsible for the VAT and show what VAT rate should be applied.

If you are a CIS contractor when you receive a bill from your CIS subcontractor you are responsible for reporting both the input and output VAT on that bill.

This change may impact your cash flow. If you are a subcontractor then it’s likely your short term cash flow will be adversely impacted as you will no longer be receiving the VAT element from your customer. If you are the contractor, you will likely have a short term cash flow benefit.

Good News

If you are on Xero, they are ready and the movement to DRC will be pretty straight forward. Once we get our heads around when we charge who for what, Xero will handle the VAT return calculations with the introduction of the new tax codes. We will make these live for you and you will see these available for use from Monday. By using these new tax codes your sales invoices will be prepopulated with the required note that no VAT is charged under the domestic reverse charge. It also applies the correct treatment itself on the return, where the amount basically goes in quite a few boxes and would otherwise give us all a headache, so thanks Xero for making this step easier!

For most, this is another scheme that you will not need to know much about. VAT loves schemes and there are quite a few around, but it is something we need to bear in mind so we are hoping this fact sheet will just make life a little easier.

Finally, we are obviously on hand if you would like to talk through any of this information or if you would like us to go through your first invoice under the scheme together please do not hesitate to contact us and we are more than happy to talk.

HMRC understands that implementing the reverse charge may cause some difficulties and will apply a light touch in dealing with any errors made in the first 6 months of the new legislation, as long as you are trying to comply with the new legislation and have acted in good faith.

If you would like to talk to HMRC their contact details are:

CIS Helpline on 0300 200 3210 (or +44 161 930 8706 if outside the UK).

VAT Helpline on 0300 200 3700 (or +44 2920 501 261 if outside the UK) for any uncertainty or clarity on whether the reverse charge applies.

Let’s understand if the work you are carrying out is subject to DRC?

When you must use the reverse charge

You must use the reverse charge for the following services:

- constructing, altering, repairing, extending, demolishing or dismantling buildings or structures (whether permanent or not), including offshore installation services

- constructing, altering, repairing, extending, demolishing of any works forming, or planned to form, part of the land, including (in particular) walls, roadworks, power lines, electronic communications equipment, aircraft runways, railways, inland waterways, docks and harbours, pipelines, reservoirs, water mains, wells, sewers, industrial plant and installations for purposes of land drainage, coast protection or defence

- installing heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems in any building or structure

- internal cleaning of buildings and structures, so far as carried out in the course of their construction, alteration, repair, extension or restoration

- painting or decorating the inside or the external surfaces of any building or structure

- services which form an integral part of, or are part of the preparation or completion of the services described above – including site clearance, earth-moving, excavation, tunnelling and boring, laying of foundations, erection of scaffolding, site restoration, landscaping and the provision of roadways and other access works

When you must not use the reverse charge

Do not use the charge for the following services, when supplied on their own:

- drilling for, or extracting, oil or natural gas

- extracting minerals (using underground or surface working) and tunnelling, boring, or construction of underground works, for this purpose

- manufacturing building or engineering components or equipment, materials, plant or machinery, or delivering any of these to site

- manufacturing components for heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems, or delivering any of these to site

- the professional work of architects or surveyors, or of building, engineering, interior or exterior decoration and landscape consultants

- making, installing and repairing art works such as sculptures, murals and other items that are purely artistic signwriting and erecting, installing and repairing signboards and advertisements

- installing seating, blinds and shutters

- installing security systems, including burglar alarms, closed circuit television and public address systems

Subcontractors – what do you need to do?

Life just got a little simpler for you! If applicable you do not need to charge VAT, you just need to state on your invoices that your customer is now liable for the VAT and you just state if this is at 20% or 5%. Do this in Xero by using the appropriate tax rate when creating a sales invoice and they does the rest! Now let’s look at who this will apply to:

The reverse charge will need to be used if you sell building and construction services when:

- your customer is registered for VAT in the UK

- payment for the supply is reported within the Construction Industry Scheme (CIS)

- the services you supply are standard or reduced rated

- you’re not an employment business supplying either staff, workers or both

- your customer has not given written confirmation that they’re an end user or intermediary supplier

If the criteria above is met – What you now need to do:

- Check if your customer has a valid VAT number.

- Check your customer’s CIS registration.

- Review your contracts to decide if the reverse charge will apply and tell your customers.

- Ask your customer to confirm whether they are an end user or intermediary supplier with a written notification, as discussed below

- Record the invoice in your accounts with the correct VAT treatment.

As a subcontractor you should also be aware that your customers will no longer be paying you VAT, which will reduce the gross value of payments coming into your business, as no VAT will be due on payments from customers where the supply is covered by the reverse charge. So you’ll need to consider and plan for the impact of this on your day-to-day cashflow. On the bright-side though, you aren’t having to worry about a large VAT bill when the VAT you have been collecting for HMRC is due!

What if the criteria is not met – Who does the reverse charge NOT apply to?

The reverse charge does not apply to any of the following customers:

- A non-VAT registered customer

- ‘End users’ i.e. a VAT registered customer who is not intending to make further on-going supplies of construction

- For reverse charge purposes consumers and final customers are called end users. They’re businesses, or groups of businesses, that are VAT and Construction Industry Scheme registered but do not make onward supplies of the building and construction services supplied to them.

- The reverse charge does not apply to supplies to end users where the end user tells their supplier or building contractor in writing that they’re an end user.

- ‘Intermediary suppliers’ who are connected e.g. a landlord and his tenant or two companies in the same group

- Overseas customers – it only applies to UK companies providing building and construction services in the UK

If you supply services that are not subject to the reverse charge, for example to private individuals or end users, you must account for VAT as you did previously, either standard 20% or reduced rate 5%.

In order to confirm if a customer falls under end user or intermediary suppliers HMRC request that you receive written notification in the form:

- on paper and sent by post

- electronically in an email

- in a contract

The notification should be kept as part of normal business records and show clearly what supplies are covered. Contracts can be either for specific supplies or it can be a Heads of Agreement or call-off type contract for supplies that are to be made at some time in the future.

If a written notification is not made correctly the customer will be liable for accounting for the VAT that should have been charged under the reverse charge. It’s important that the person making the notification knows and understands that it’s correct.

An example of the wording to obtain for the written notification is:

‘We are an end user for the purposes of section 55A VAT Act 1994 reverse charge for building and construction services. Please issue us with a normal VAT invoice, with VAT charged at the appropriate rate. We will not account for the reverse charge.’

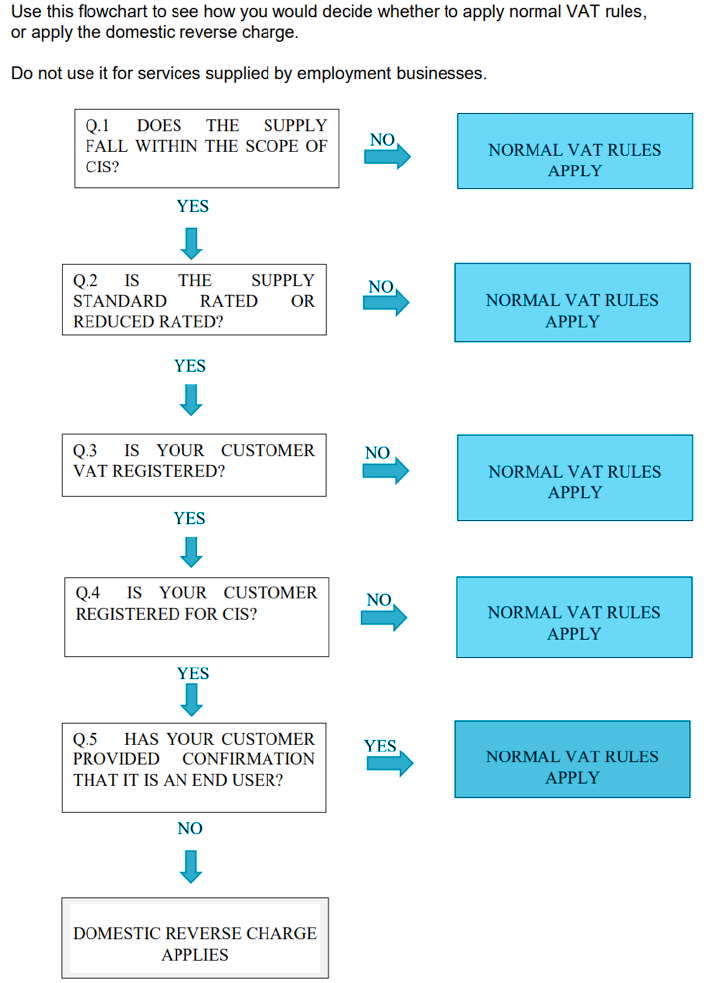

The below flowchart has been provided by HMRC to help determine whether the supply is DRC or normal VAT rules applies:

Contractors – what do you need to do?

Life just got a little better for you, you should notice the difference of the scheme with a short term cashflow boost. If applicable, subcontractors will not be charging you VAT so you will not be paying it over to them when settling their invoice (everyone likes to hold on to their cash a little bit longer)!

The reverse charge will need to be used if you buy building and construction services when:

- payment for the supply is reported within the Construction Industry Scheme (CIS)

- the supply is standard or reduced rated

- are not hiring either staff or workers, or both

- you’re not using the end user or intermediary exclusions

If you receive a service subject to the reverse charge from subcontractors you’ll have to account for the VAT in your VAT Return and recover it simultaneously on the same VAT Return, subject to the normal rules on VAT input tax deduction.

If the criteria above is met – What you now need to do

- Check if your supplier has a valid VAT number.

- Tell your supplier if you’re an end user or intermediary supplier, as the reverse charge will not apply.

- Find out how to account for the charge.

Once you’ve confirmed your accounting systems and software can account for the reverse charge, you’ll need to:

- make sure the invoice you receive is correct

- check the list of services that must use the reverse charge

- record the reverse charge on your VAT return and reclaim it in the usual way

The Reverse charge does not apply to any of the following supplies:

- Supplies of VAT exempt building and construction services

- Supplies that are not covered by the CIS, unless linked to such a supply

- Supplies of staff or workers

The Reverse charge does not apply to any of the following customers, you as a contractor to a subcontractor:

- A non-VAT registered customer

- ‘End users’ i.e. a VAT registered customer who is not intending to make further on-going supplies of construction

- For reverse charge purposes consumers and final customers are called end users. They’re businesses, or groups of businesses, that are VAT and Construction Industry Scheme registered but do not make onward supplies of the building and construction services supplied to them.

- The reverse charge does not apply to supplies to end users where the end user tells their supplier or building contractor in writing that they’re an end user.

- ‘Intermediary suppliers’ who are connected e.g. a landlord and his tenant or two companies in the same group

- Overseas customers – it only applies to UK companies providing building and construction services in the UK

Telling your supplier (subcontractor) that you are an end user or intermediary supplier:

In order to confirm if you as a customer fall under end user or intermediary suppliers, HMRC request that you provide written notification in the form:

- on paper and sent by post

- electronically in an email

- in a contract

The notification should be kept as part of normal business records and show clearly what supplies are covered. Contracts can be either for specific supplies or it can be a Heads of Agreement or call-off type contract for supplies that are to be made at some time in the future.

If a written notification is not made correctly the customer (you) will be liable for accounting for the VAT that should have been charged under the reverse charge. It’s important that the person making the notification knows and understands that it’s correct.

An example of the wording to use for the written notification is:

‘We are an end user for the purposes of section 55A VAT Act 1994 reverse charge for building and construction services. Please issue us with a normal VAT invoice, with VAT charged at the appropriate rate. We will not account for the reverse charge.’

The subcontractor should report on their invoice to you what rate the reverse charge is applicable, please be aware this can be standard 20% or reduced rate 5% depending on the service and supply.

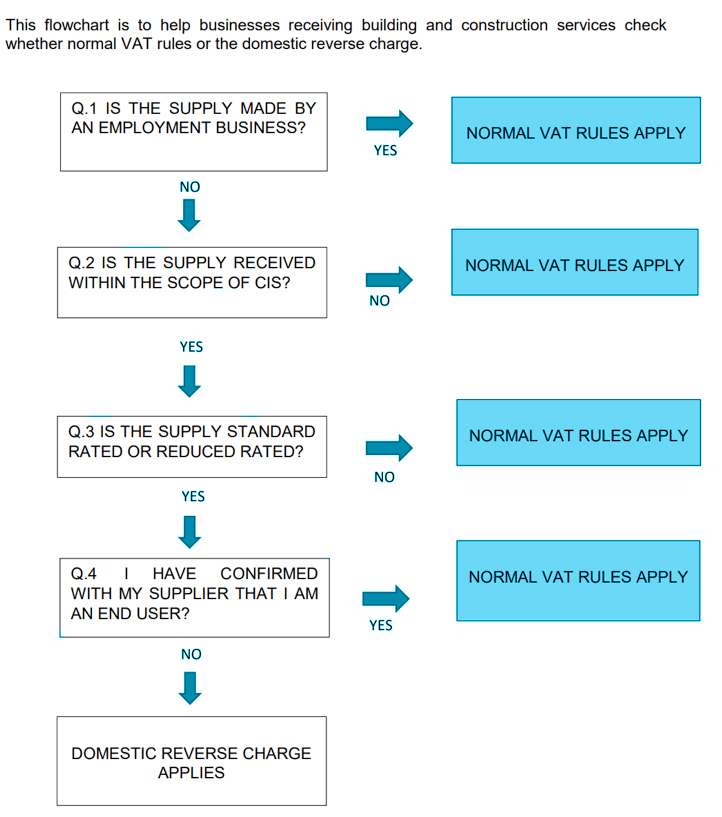

The below flowchart has been provided by HMRC to help determine whether the supply is DRC or normal VAT rules applies:

Are you using the Cash Accounting Scheme or Flat Rate Scheme?

You cannot use the VAT Cash Accounting Scheme for supplies of services that are subject to the reverse charge – VAT is due when a VAT invoice is issued (tax point) or the payment is received, whichever is earlier.

Reverse charge supplies are not to be accounted for under the Flat Rate Scheme. Flat Rate Scheme users who receive reverse charge supplies will have to account for the VAT due to HMRC and recover it simultaneously on the same VAT Return. Users of the Flat Rate Scheme will have to consider if it’s still beneficial to them bearing in mind that under the scheme they cannot recover VAT incurred on purchases of materials, overheads and so on.

Useful links

HMRC Guidance – they are the ones to set these rules I suppose! This link is useful for ver specific matters too like new builds, joint ventures, local authorities and utilities (the list goes on): https://www.gov.uk/guidance/vat-reverse-charge-technical-guide#flowcharts

Xero – If you are with Xero, they have your back, the software deals with all the legalities: https://www.xero.com/uk/features-and-tools/accounting-software/domestic-reverse-charge/

Link to check for valid CIS registration: https://www.gov.uk/use-construction-industry-scheme-online

Link to HMRC list of services, included above, but subject to updating, it is worth to reference the source document: https://www.gov.uk/guidance/vat-domestic-reverse-charge-for-building-and-construction-services#whentouse

If your business could use the Cypher touch, please contact us and we will be happy to discuss your options.